It’s imperative to measure your day trading performance if you want consistent long-term gains.

A lot of top forex traders avoid the topic of measuring their trading performance which every top FX trader must know how to do. You need to spend time researching trading performances since it plays a crucial role in formulating your trading strategy. Most forex traders tend to measure their trading performance in terms of losses and dollars made. The bottom line is going to be the ultimate score when measuring your performance in dollars.

However, that doesn’t give you the real picture of your trading strategy, and it is imperative that you measure your day trading performance through other metrics if you want consistent long-term gains. Evaluating and understanding the performance of your trading system will help you avoid costly mistakes and get the right results. A lot of traders don’t completely understand how to interpret their trading results and risk properly, which stops them from becoming the best forex trader they can be.

Definition of Trading Performance

You can express trading performance in several forms and complex algorithms, and it is technically the mechanism that helps evaluate a trader’s risk tolerance and return or lack thereof. You can measure all types of trading performance, whether it is for swing traders, day traders, and all the rest. The most challenging thing about measuring trading performance is making sense of all the measurement approaches and numbers, which is what we will be discussing below.

There are a lot of different metrics and statistics that help measure performance for traders, and the most common statistics used for measuring trading performance over time are as follows:

Absolute Drawdown

What is Absolute Drawdown?

Absolute drawdown is known as the difference between the minimal point below the deposit level and the initial deposit, during the testing period. It shows you how big your loss will become compared to the initial deposit when trading. If the value was 0 during the test, your deposit wasn’t at risk.

Relative Drawdown

What Is Relative Drawdown?

Relative drawdown is known as the highest Max-Drawdown in percentage in the test period.

For instance: You start with $10,000, and on your first trade your equity goes down to $9,500, meaning you suffered a 5% loss in percentage. The maximum drawdown and relative drawdown will lock that as the highest draw-down it’s ever seen in percentage. Then your trading turns around and you profit $1,500. Now your account worth is $11,500. On your next trade, you have lost $2,000. Now your account worth is $9,500. While the absolute drawdown would be $10,000 – 9,500 which is only 5% absolute drawdown, the relative drawdown would be from the peak highest value of the account $11,500 minus the lowest unrealized value of the account, which is 9,500, which is equal to $2,000 in relative drawdown.

Click to learn more about Drawdown in Forex, and how it makes you a better trader.

Profit Factor Measures

What is a Profit Factor?

The third common metric for measuring trading performance is the profit factor. It calculates the total of your winning trades and divides it with the total value of your losing trades to determine profitability.

It is calculated in terms of R since it helps you check the amount of money you make relative to your losses, irrespective of the number of trades. For instance, If you have a winning percentage of 40%, but your wins are bigger than your losses, you will still turn up a profit. The table below accurately illustrates this point:

| 8000 | Winner |

| 3500 | Winner |

| 5400 | Winner |

| -2500 | Loser |

| -4500 | Loser |

| 3000 | Winner |

| -800 | Loser |

| -734 | Loser |

| -2000 | Loser |

| -1500 | Loser |

| 10 Total Trades | |

| 4 Winner | 19900 |

| 6 Losers | 12034 |

| R= | 1.65 |

The table above shows that you still managed to turn a profit, even though you had more losses than wins. It showed that you are still 65% more profitable on your winning trades, and therefore managed to land in the black.

Here you can find a great example of a money management strategy called The Lower Hanging Fruit

Standard Deviation Measures

What is Standard Deviation?

Standard deviation is recognized as the statistical measure of market volatility, which measures how widely prices are dispersed from the average price. If prices were trading in a narrow trading range, the standard deviation will show a low value, indicating low volatility. However, if prices swing up and down, then the standard deviation will show a high value, indicating high volatility.

Standard deviation is one of the most important tools used in trading and investing strategies, since it measures market volatility, security, and predicts trading performance trends.

When it comes to investing, an index fund will have a lower standard deviation than its benchmark, because the goal of the fund is to replicate the index. However, you can also expect aggressive growth funds to have high standard deviations compared to stock indices because portfolio managers made aggressive bets to help generate above-average returns.

A low standard deviation isn’t the best for trading, but that depends on the investments you are making and the risk you are willing to assume. When dealing with deviation in your portfolio, you must consider your overall investment objective and your tolerance for volatility.

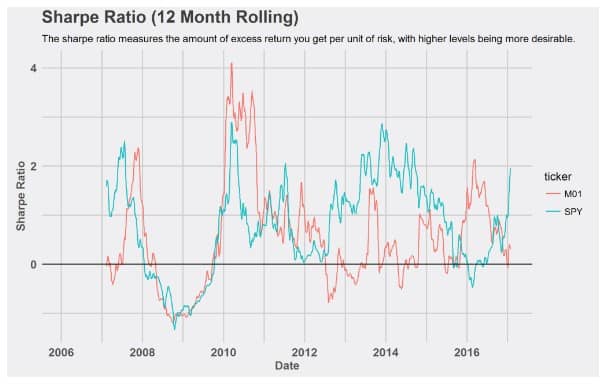

Sharpe Ratio Measures

What is Sharpe Ratio?

The Sharpe ratio is designed to measure the risk-adjusted performance of a strategy. The ratio is reported by asset managers and offers an easy way to compare performance between strategies. It has several variations in calculating the Sharpe ratio, but the common is the excess return of the strategy, divided by the standard deviation of the returns. The interpretation of the ratio is the total excess return you get per unit of risk. Higher levels are more desirable.

The graph below plots the 12-month rolling Sharpe ratio for the strategy and sets the benchmark. I have smoothed the Sharpe ratio to make the interpretation clearer.

The interpretation is that the M01 strategy managed to outperform the benchmark rarely, and the period from 2012 to 2016 was underperformance. The Sharpe ratio doesn’t apply when excess returns are negative because low volatility, creates a negative Sharpe ratio. There are several other risk-adjust measures, but most of them attempt to find the same thing. The ratios are used commonly to compare strategies and let others know whether a trading strategy is effective or not for use in their trading plan.

Learn more about the trading ratio

Measure Your Trading Performance – the Bottom Line

You have to measure and back-test your trading strategy, this is one of the keys to becoming a profitable trader.

You shouldn’t limit yourself to measuring your system for only 1 year or for 100 trades.

Always measure your strategy, especially if you decided to change one of the indicators.